I still have the preliminary 2026 rate filings to analyze for about 10 more states, but I'm taking a break to go back and revisit ARKANSAS.

Back on July 18th, I posted my original analysis of ACA-compliant individual & small group market filings for Arkansas insurance carriers. At the time, I found that the weighted average increases being requested for individual market policies averaged a disturbingly high 26.2%. Here's what the breakout looked like:

Oregonians continue to have at least five health insurance companies to choose from in every Oregon county as companies file 2026 health insurance rate requests for individual and small group markets

In-depth rate review process just beginning, opportunities for public review and input remain through June 20

June 2, 2025

Oregon health insurers have submitted proposed 2026 rates for individual and small group plans, launching a months-long review process that includes public input and meetings.

Five insurers will again offer plans statewide (Moda, Bridgespan, PacificSource, Providence, and Regence), and Kaiser is offering insurance in 11 counties, giving six options to choose from in various areas around the state.

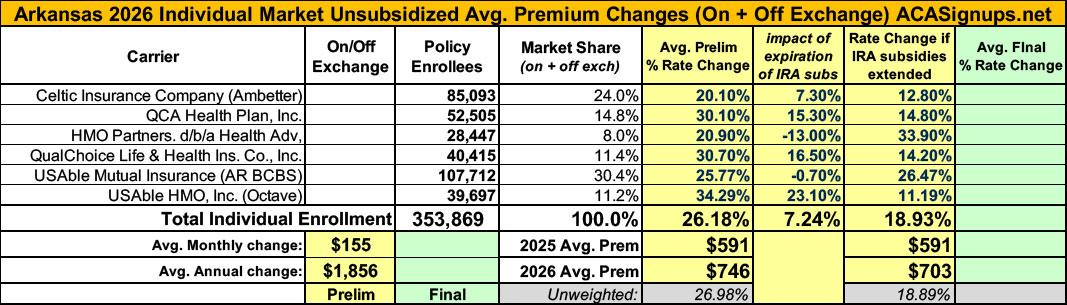

(sigh) OK, I'm not sure if we've reached the 5th or 6th chapter in this ongoing saga, but I hope it's the last one.

When we last left our story (just 5 days ago), I noted that both the current number of enrollees as well as the average rate increases for each of the carriers on the Arkansas individual market had jumped all over the place at least 4 times, and that while it's common for these numbers to change a bit here and there throughout the multi-month filing process, both the degree of some of the changes as well as the circumstances surrounding them were often far beyond what I've typically seen in over a decade of tracking this stuff:

Given all the confusing numbers I've posted before, I've boiled it all down to the simplified tables below which illustrate the mess:

I already wrote about this over a month ago but it didn't get the attention it deserved at the time, and given that we're much closer to the actual 2026 ACA Open Enrollment Period starting and that there's been another important development since then, I figured I should post an updated entry about it.

Santa Fe, NM – The New Mexico Office of the Superintendent of Insurance (OSI) has approved 2026 rates for individual market Affordable Care Act (ACA) plans sold on and off BeWell, the New Mexico Health Insurance Marketplace, with an average increase of 35.7%. Today, 75,000 New Mexicans buy health insurance through BeWell and 88% of enrollees qualify for federal and state premium assistance.

(Aetna/CVS is pulling out of the entire individual market nationally)

Anthem Blue Cross of CA (DMHC)

This is a rate filing for the Individual market ACA‐compliant plans offered by Anthem Blue Cross (Anthem). The proposed rates in this filing will be effective for the 2026 plan year beginning January 1, 2026, and apply to plans both On‐Exchange and Off‐Exchange.

Anthem will continue to participate in its 2025 marketplace footprint consisting of rating areas 1-10 and 12-14 with EPO plans and rating areas 11 and 15‐19 with HMO plans.

The projected average rate change for plans effective January 1, 2026 is 16.0% which is an average rate change of about $87 per member per month (pmpm). Because 16.0% (or about $87) is an average, it is possible to have a different rate change. Factors affecting a member's premium are age, tobacco use, family composition, plan, and geographic area. Expected cost differences by product are updated every year to ensure premium differences are appropriate. BridgeSpan has approximately 200 members enrolled in this line of business as of March 2025.

...The rate change described above is driven by the following factors:

Medical Trend : 9.1%

Change in Benefits, Age, Area, and Network : -1.5%

Change in Market Morbidity : 5.0%

Exchange User Fees : 1.0%

Other : 2.0%

Other includes: actual results vs. expected, changes to admin expenses, and rx rebates. Actual results vs. expected reflect differences between actual results and past assumptions, including a true-up of market morbidity estimates

In the most recent chapter of the ongoing 2026 Arkansas rate filing saga, I noted that both the total number of residents enrolled in ACA individual market policies as well as the average 2026 rate increases for the six insurance carriers participating in the individual market next year kept changing, often in ways which were contradictory with other numbers claimed within the same press releases:

You'll notice that in addition to the rate changes being updated (increasing from a weighted average hike of 26.2% to 35.7%), most of the current enrollee figures were also modified, although these only changed slightly in most cases. Overall the total number of current individual market enrollees statewide dropped a bit from ~354,000 to ~345,000.

Minor changes like this aren't unusual; sometimes the carriers make slight tweaks as more recent data comes in or clerical errors are corrected; other times they round off the enrollee totals (that doesn't seem to be the case here, however).

Iowa Code §505.19 requires the Commissioner to hold a public hearing on a proposed individual health insurance rate increase which exceeds the average annual health spending growth rate as published by the Centers for Medicare and Medicaid Services of the United State Department of Health and Human Services. For 2026 the growth rate is 5.6%.

The Iowa Insurance Commissioner will hold a public hearing regarding the relevant rate increases on August 19, 2025.

The purpose will be to hear public comments on the proposed increase in the base premium rate. Consumers wishing to make a public comment at the hearing are encouraged to attend the hearing via the live webcast.

All comments received will be considered public records and will be posted here. The Consumer Advocate will present the public comments received at the hearing.

Every year, I spend months painstakingly tracking every insurance carrier rate filing (nearly 400 for 2025!) for the following year to determine just how much average insurance policy premiums on the individual market are projected to increase or decrease.

Carriers tendency to jump in and out of the market, repeatedly revise their requests, and the confusing blizzard of actual filing forms sometimes make it next to impossible to find the specific data I need.

I really only need three pieces of information for each carrier:

Federal policy shifts drive higher 2026 rates for individual and small group health plans

State actions blunt increases tied to the reconciliation bills and policy direction of the federal government

St. Paul, MN: Health insurers have submitted their proposed increased rates to the Minnesota Department of Commerce for 2026 plans available to Minnesotans who buy individual or small group health insurance through MNsure or directly through insurers. These proposed rates apply to coverage starting Jan. 1, 2026, with open enrollment beginning Nov. 1, 2025.