How much more are ~200,000 NEW YORK ACA enrollees *really* paying this year due to Trump/GOP policies?

WARNING: This one gets complicated. REALLY complicated.

IMPORTANT: See the original post in this series for an explanation of the methodology.

Regular readers know that I've been obsessing over the massive increases in both gross as well as net premiums for ACA health insurance policy enrollees being caused by the combination of Congressional Republicans allowing the enhanced federal tax credits to expire as well as other Trump Regime policy changes for well over a year and a half now.

I've written countless analyses of how much both gross and net premiums skyrocketed from 2025 to 2026 across different states, different income levels and various other demographics...and last week it was revealed that over 3 million ACA exchange enrollees had already been priced out of the market as of April, with the number almost certain to climb further throughout the rest of 2026.

As I've repeatedly warned, however, the increases in premium costs (whether gross or net) are only half the story. The other big shoe which is dropping this year is increased out of pocket costs as millions of the ~19.2 million or so remaining enrollees as of April have been forced to downgrade their coverage to avoid (or at least minimize) those massive premium spikes.

In most cases this means moving to plans with higher deductibles, higher co-pays & higher coinsurance costs. In many cases this has also included moving to plasn with worse networks, referral requirements to see specialists and so on.

With that in mind, that's exactly what I've decided to set out to do: Calculate the average year over year increase not just in net premiums (that is, how much more ACA enrollees are having to pay each month) but also the year over year change in average out of pocket costs.

IMPORTANT: Those who have been following this state-by-state series know that most of them are laid out & phrased almost identically aside from the actual data & graphics. This one, for New York, will include the same tables & graphs...but has some VERY important caveats.

Let's look at NEW YORK:

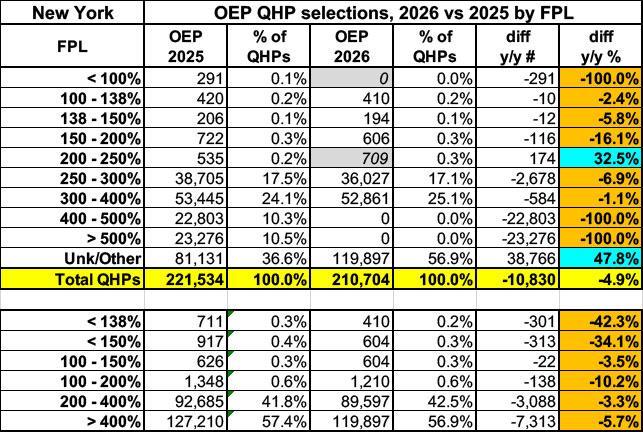

Here's a look at ACA exchange plan selections during Open Enrollment by household income level this year vs. last.

- Caveat #1: All of the data below is based on plan selections during the Open Enrollment Period (OEP) only, which was down around 5% vs. the 2025 OEP. As of May 2026, effectuated ACA enrollment in New York's individual market was actually down 8.7% year over year, and down around 7% on average per month.

- Caveat #2: Like the District of Columbia and Minnesota, New York also has a Basic Health Plan program in place...and while both of those BHP programs enroll residents earning up to 200% of the Federal Poverty Level (FPL), a couple of years back New York overhauled & expanded their BHP program (called "The Essential Plan") to include residents who earn up to 250% FPL.

This significantly boost enrollment in the program, of course...which also means that it decreased enrollment in official ACA exchange policies by shifting practically everyone earning less than 250% FPL over to it...which in turn had a profound skewing effect on average premiums, metal level/actuarial value breakout and so on for the remaining enrollees.

You can clearly see this in the first table below, which only lists around ~2,000 NY enrollees earning below 250% FPL in either year:

It's also worth noting that according to the official CMS Public Use File, enrollment over 400% FPL has not only dropped dramatically, as you would expect...it's supposedly dropped off to nothing at all, which is extremely unlikely. The official data claims that all ~46,000 in this income bracket last year have dropped coverage...but it also claims that enrollees with "Unknown/Other" incomes have increased by nearly 39,000 people this year, which means it's extremely likey that the powers that be at NY State of Health simply recategorized anyone earning more than 400% FPL as "Unknown/Other" since they're no longer eligible for financial assistance anyway.

In any event, overall, nearly 11,000 New Yorkers lost ACA coverage during Open Enrollment alone, and since then the year over year drop has grown to over 14,000.

Onto the main analysis:

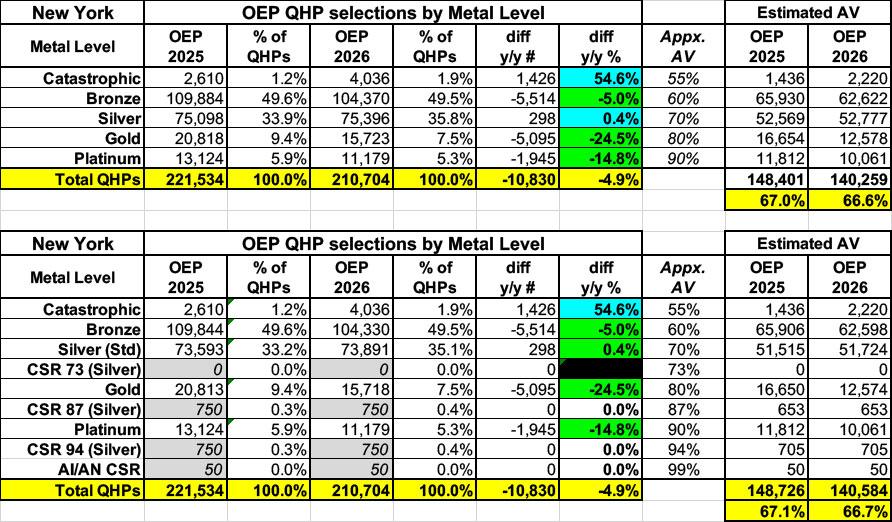

Here's total Open Enrollment plan selections for both 2025 & 2026 broken out by Actuarial Value (AV) category. The first table is based on official metal level tiers, but it's the second table which is critical, since a huge chunk of ACA enrollees are usually enrolled in CSR Silver plans (which include Cost Sharing Reduction assistance). CSR assistance dramatically boosts the AV of Silver plans up to Platinum levels in most cases.

- Caveat #3: Officially, the CMS Public Use File claims that 45,169 of those who selected plans during OEP this year receive CSR assistance, compared to 41,504 receiving CSR help last year. HOWEVER, this makes ZERO sense for two reasons:

- First: As noted above, due to the (expanded) BHP program, only around ~2,000 exchange enrollees earned less than 250% FPL either year to begin with; and

- Second: According to a companion CMS Public Use File, there were only around ~1,500 exchange enrollees in New York who a) earn less than 250% FPL and b) selected Silver plans...which are the only plans available with CSR assistance unless you're a member of an American Indian tribe or an Alaska Native.

Well, it turns out that (h/t to my colleague Louise Norris for this!), deep inside the CMS Public Use File definitions, it states that for New York only:

...New York's count of consumers with APTC and CSR includes a subset of consumers receiving state cost-sharing subsidies under an approved section 1332 waiver.

I'll explain what this is talking about below, but the point is that the ~45K (or least year's ~41K) "CSR enrollees" is, for the most part, not referring to federal CSR enrollees.

WITH THAT IN MIND, I'm using far more realistic estimates of the CSR category breakout below: The overall Actuarial Value of New York enrollees dropped slightly from 67.1% to 66.7%.

Enrollment in Platinum and Gold plans has dropped substantially, while Silver & Bronze stayed pretty mcuh the same...but Catastrophic enrollment jumped by more than 54% year over year. In raw numbers, however, this is only a ~1,400 increase.

In other words, unlike most states, in New York's case most enrollees either stayed pretty much where they were...or dropped coverage altogether, at least during Open Enrollment:

IMPORTANT: I only have detailed CSR category enrollment data for the 30 states hosted via the federal ACA exchange, HealthCare.Gov. Unfortunately, the Centers for Medicare & Medicaid Services (CMS) only provides total CSR enrollment for most of the 21 state-based exchanges (SBEs).

For these states, which includes New York, I'm instead relying on rough estimates based on the percent of enrollees in the 100 - 150%, 150 - 200% and 200 - 250% FPL income brackets who selected Silver plans each year, which can be found in the 2025 & 2026 OEP State, Metal Level, and Enrollment Status Public Use Files (ZIP) from CMS.

These percentages, when converted into raw numbers, correspond fairly closely to the actual CSR category breakouts for FFM states (+ or - 5%), so they should be close enough for my purposes. I've also come up with rough estimates for the AI/AN CSR category based on comparisons of the percent of AI/AN CSR QHPs selected in FFM states to the percent of AI/AN residents within each state. This is less than 3.3% in every SBE state except for New Mexico.

Again, these are broad estimates only but should be reasonably accurate for this project.

By combining these numbers with the average gross premiums per enrollee I'm able to calculate an estimate of the average total medical expenses each enrollee racks up each year assuming an 80% average Medical Loss Ratio (as I stated in the original post, this can vary widely by carrier and year, so should be considered a very broad average only).

HOWEVER, this also brings up...

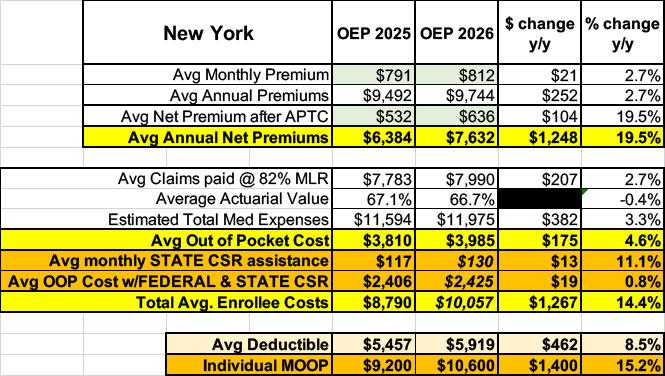

- Caveat #4: In addition to expanding their BHP program to include residents earning up to 250% FPL, New York State also included their own Cost Sharing Reduction (CSR) assistance specifically for exchange enrollees who earn between 250 - 400% FPL both last year and this year!

- While I don't know the exact per enrollee dollar amount, according to their letter to then-HHS Secretary (and current Democratic nominee for Governor of California) Xavier Becerra back in April 2024, they were projecting the state CSR program to cost roughly $303 million in 2025 and perhaps ~$310 million or so in 2026.

Based on the average monthly enrollment each year, this breaks out to roughly $117/month per enrollee in 2025 and around $130/month apiece this year, giving a table like so:

Overall, to the best of my calculations & estimates, New York ACA exchange enrollees are paying around $100 more per month in net premiums apiece on average, or $1,200 more this year than last. That's roughly a 20% net increase.

The good news (such as it is) is that thanks to the extra state CSR assistance, their out of pocket expenses seem to only have gone up modestly, for a combined average healthcare cost increase of around ~14.4% (a little under $1,300 more apiece, give or take).

EXCEPT...this brings me to...

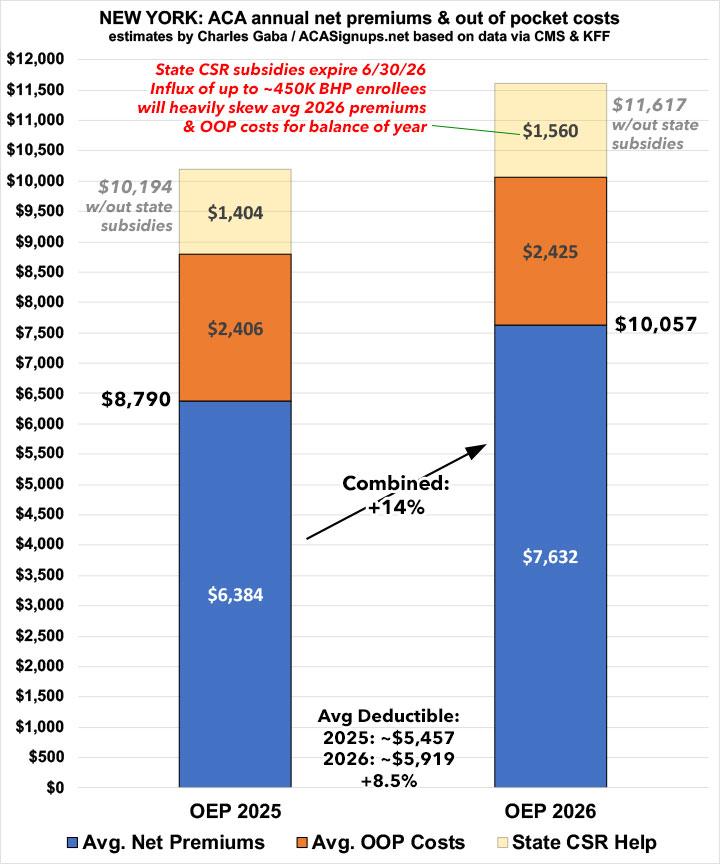

The same waiver which New York used to expand eligiblity in their BHP program from 200% FPL to 250% FPL also included the ~$300M/yr in state CSR assistance...and with the waiver being terminated, not only will up to 450,000 Essential Plan enrollees lose coverage effective July 1st (just a week or so from today), but the CSR help will be going away as well.

The thing is...I don't know whether they're cutting the CSR assistance off on July 1st as well, or if they'll be able to keep it going for the rest of 2026.

In any event, the bar graph below is my best attempt to visualize the situation...with the major caveat that the ~$1,560/enrollee in average CSR assistance may no longer apply in just over a week.

Anyway, based on KFF's net data, average deductibles also increased by ~8.5% to ~$5,900 for single coverage this year, and the maximum (theoretical) out of pocket cut-off for all ACA enrollees went up by over 15% this years as well, to $10,600 for single coverage.

Next up: NORTH CAROLINA.

Advertisement