2027 Rate Changes - Maryland: +13.7% indy, +13.1% sm. group

Fri, 06/26/2026 - 1:42pm

via the Maryland Insurance Administration:

Health Carriers Propose Affordable Care Act Premium Rates for 2027

Proactive policies of the Moore Administration and General Assembly ensure that Maryland's individual premium rates remain among the lowest in the nation, in spite of federal pressures due to changing Exchange rules and continued lack of expansion of enhanced tax credits

BALTIMORE – The Maryland Insurance Administration has received the 2027 proposed premium rates for Affordable Care Act products offered by health and dental carriers in the individual, non-Medigap and small group markets, which impact approximately 482,000 Marylanders and represents 19% of the commercial health insurance market.

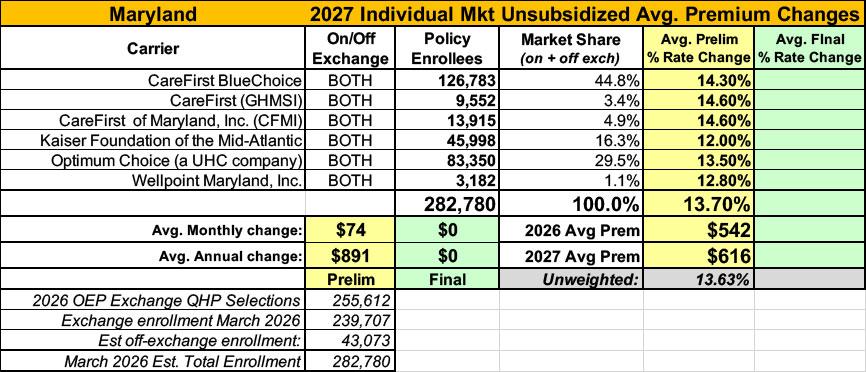

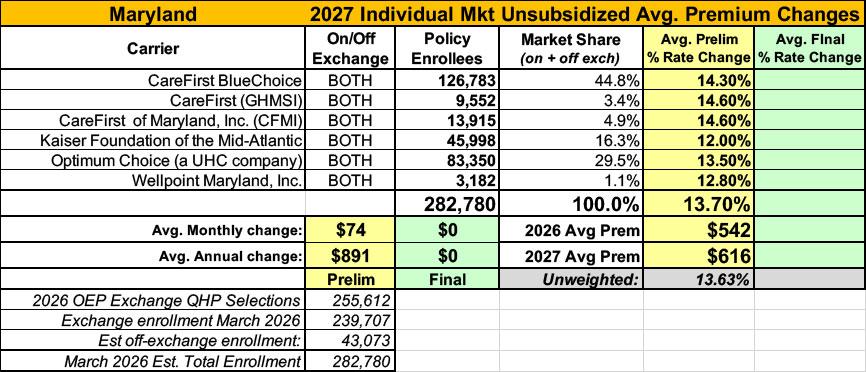

In the individual, non-Medigap market, carriers are requesting an overall average rate change of 13.7%, with the average request by carrier ranging from 12% to 14.6%.

“The significant rate increases filed with the Maryland Insurance Administration for the second year in a row reflect the loss of enhanced federal tax credits, which were not extended by Congress and the Trump Administration last year,” said Maryland Insurance Commissioner Marie Grant. “Without the proactive steps by Governor Wes Moore and the Maryland General Assembly to enact a state-based subsidy for 2026 and 2027, Marylanders would see significantly higher increases in premiums and out-of-pocket costs. Our team of actuaries will closely examine the assumptions behind the rate requests over the coming months to determine whether they are justified.”

According to health information company KFF, in the individual market, Maryland has the lowest-cost average bronze-level premium and the lowest-cost average gold-level premium in the country in 2026. Maryland's lowest-cost silver-level average premium is second only to New Hampshire.

Sidenote: According to my data, Idaho actually has the lowest average 2026 gross premiums overall, with Maryland coming in third after Idaho & New Hampshire...although it's a close third.

Under the leadership of Governor Wes Moore, Maryland created a new subsidy program through the Maryland Health Connection for those who are under 400% of the federal poverty level to help offset the expiration of the enhanced federal tax credit subsidies. The state subsidy program replaced 100% of the enhanced federal subsidies for those under 200% of federal poverty level and replaced 50% of the enhanced federal subsidies for those between 250% and 400% of the federal poverty level for 2026.

Sidenote: I originally thought this was a typo since it doesn't mention those earning 200 - 250% FPL, but it turns out the state subsidy gradually tapers off from 100% to 50% of the lost federal tax credits over that income range.

The subsidy is expected to continue for 2027, although the exact amount will depend on a number of variables. For example, the Health Services Cost Review Commission is reviewing a recommendation that would fund additional support for market stability.

More specifically, for 2027, it looks like Maryland is considering three options, one of which would be identical to this year, one which would only cover 25% of the lost subsidies for those earning 250 - 400% FPL, and one of which would only cover 25% from 250 - 400% FPL while also eliminating their other subsidy program for young adults.

Maryland’s rates in the individual market also remain low compared with the rest of the nation because of the continued effectiveness of the state’s 1332 State Innovation Waiver in stabilizing the market. The 1332 waiver is approved by the federal U.S. Centers for Medicate and Medicaid Services (CMS) through 2028.

The carriers’ requested increases are reviewed by the Maryland Insurance Administration and rates must be approved by the Commissioner before they can be used. Before approval, all filings undergo a comprehensive review of the carriers’ analyses and assumptions. By law, the Commissioner must disapprove or modify any proposed premium rates that are unfairly discriminatory or appear to be excessive or inadequate in relationship to the benefits offered.

The Insurance Administration will hold a public hearing on the ACA proposed rates on July 23, 2026, and expects to issue decisions in September 2026.

Small Group Market

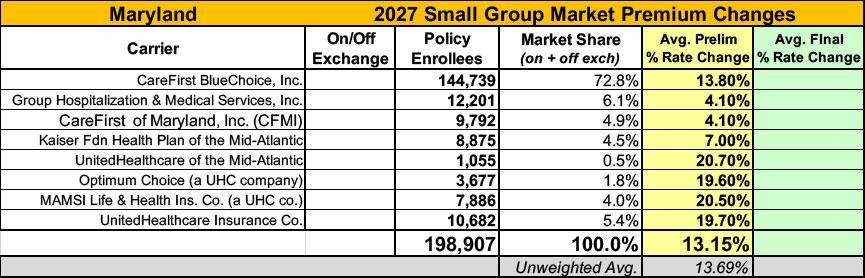

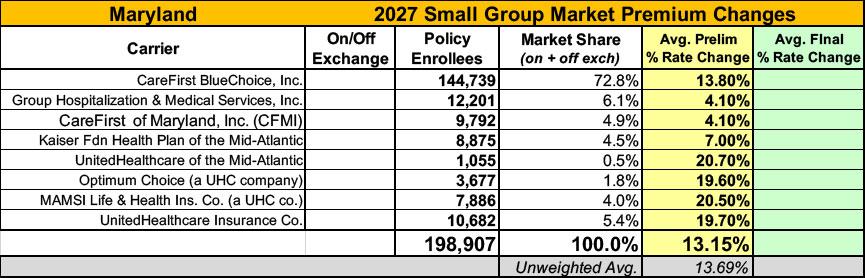

In the small group market, carriers have requested an overall average rate increase of 13.1%, with the averages by carrier ranging from 4.1% to 20.7% for 2027, reflecting increased utilization of health care services across both medical and drug service categories. These trends are happening nationally as well as in Maryland.

For 2026, the Insurance Administration has approved mid-year rate changes for CareFirst BlueCross BlueShield and UnitedHealthcare products in Maryland’s small group market, because of evidence of a significant increase in in-patient hospitalizations and in-patient and out-patient surgeries.

Notably, the current approved average rates are 2.1% lower than requested for CareFirst BlueCross BlueShield and 6.4% lower than requested for UnitedHealthcare. The Insurance Administration approved an average mid-year adjustment of 5.6%, resulting in an annual rate increase of 8.2% for the third quarter of 2026 and an average annual rate increase of 8.6% for the fourth quarter for the CareFirst Blue Choice Inc. product. The Administration approved a mid-year adjustment of 1.5% for United Healthcare effective October 1, affecting about 26,200 members and resulting in a 10.1% annual increase.

“The Maryland Insurance Administration is required to consider mid-year Affordable Care Act rate adjustments by carriers serving small businesses based on changes in the market,” Commissioner Marie Grant said. “Our team carefully analyzed the requests and determined that some level of rate changes were justified based on significantly higher than expected claims and health care costs. However, the increases that were approved were less than what the carriers originally requested after actuarial review.”

The Maryland Insurance Administration, in partnership with the Maryland Health Benefit Exchange, will hold a meeting later this summer to discuss options to increase access for comprehensive health coverage for small employers. With the rising cost of health insurance, some small businesses in Maryland are opting for a higher risk health insurance option called a “level-funded health plan.” This type of group health plan may offer lower premiums that appear more affordable, particularly if groups are healthy. The reason for the potential lower rates is that these arrangements rate on health status, which is prohibited in the fully-insured small group market. However, it is important for employers to know that level-funded health plans are, in part, a type of self-insured arrangement and bring other duties and obligations for the employer. It is also important to know that level-funded health plans lack many of the protections fully insured plans have under Maryland law.

The Insurance Administration held public hearings in April and May on the requests, which were extensively reviewed by the Office of the Chief Actuary.

The Insurance Administration will hold a quasi-legislative virtual public hearing on all proposed 2027 rates at 1 PM on Thursday, July 23, 2026.

(See public hearing details below.)Summary of Proposed Rates for 2027

For the individual, non-Medigap market, the overall filed average annual rate change across the entire market is an increase of 13.7%. The average filed rate by carrier and the number of impacted members based on enrollment as of April 30, 2026, is:

...Additional details regarding proposed rate changes in the individual market are provided in Exhibit 1. Additional premium comparisons for bronze and gold and for an illustrative family of four are found in Exhibit 2.

Note that all illustrative premiums are the full unsubsidized premiums prior to the application of any Advance Premium Tax Credits (APTCs) from the federal government or the state young adult subsidy. Almost 70% of applicants who purchase a plan on www.marylandhealthconnection.gov receive subsidies and will not pay the full premiums shown here. Subsidies vary by a household’s income and are linked to the unsubsidized cost of the second lowest cost silver plan available to a household.

For the small group (50 or less full-time equivalent employees) market, the overall filed average annual rate change is an increase of 13.1%. In the small group market, a health carrier can request rate changes on a quarterly basis. The proposed average rate changes by carrier for all four quarters of 2027 and the number of impacted members based on enrollment as of March 31, 2026 is:

...Additional details regarding these proposed rate changes are provided in Exhibit 3. Additional premium comparisons for bronze and gold and for an illustrative familiy of four are found in Exhibit 4.

In the individual, non-Medigap, stand-alone dental market, carriers have requested an overall average increase of 6% with averages by carrier ranging from no increase to 19.8%. In addition, a new dental carrier, Best Life and Health Insurance Company, has filed rates for new plans that will be available in 2027. The average filed rate by carrier and the number of impacted members based on enrollment as of April 30, 2026 is:

- Alpha Dental: DPPO 6,034 0.0%

- CareFirst GHMSI/CFMI: DPPO 56,476 1.4%

- Delta Dental: DPPO 28,262 10.4%

- Dominion Dental: DHMO & DPPO 12,191 19.8%

Additional details regarding these proposed rate changes are provided in Exhibit 5. Illustrative premiums for both Self-Only and Family coverage can be found in Exhibit 6.

Rates being reviewed by the Insurance Administration do not affect health insurance plans offered by large employers or by employers who self-insure; “grandfathered” plans purchased before March 2010; or federal plans such as Medicare (including Medicare Advantage or Medicare Supplement), Tricare and federal employee plans.The six exhibits listed below provide more detail. Read EXHIBIT list.

- EXHIBIT 1: 2027 ACA, Individual Non-Medigap Market – Rate Filing Summary

- EXHIBIT 2: Illustrative Individual Non-Medigap 2027 Premiums

- EXHIBIT 3: 2027 ACA, Small Group Market – Rate Filing Summary

- EXHIBIT 4: Illustrative Small Group 2027 Premiums

- EXHIBIT 5: 2027 ACA, Individual Non-Medigap, Stand-Alone Dental Market – Rate Filing Summary

- EXHIBIT 6: Illustrative Individual Stand-Alone Dental 2027 Premiums

Rate filing documents are available on the Insurance Administration’s website, which also includes answers to frequently asked questions about the rate review process. All interested persons may review filings and submit comments through Aug. 28, 2026.

In addition, any interested person may participate in the virtual public hearing scheduled for July 23, 2026. Time limits may be imposed for oral testimony, depending on the number of participants. If you would like to present or offer public comments during the public hearing, please notify the Insurance Administration in advance by submitting your request to healthinsuranceratereview.mia@maryland.gov. To the extent that time and technology permit, the Insurance Administration will hear from unregistered participants who access the Zoom Webinar platform.

Public Hearing Log-In Information:

- When: 1 PM to 3 PM, Thursday, July 23, 2026

- ZoomGov Link

- Dial-In: (646) 828-7666

- Webinar ID: 165 673 0683

Written testimony for the public hearing may be submitted by email and must be received by Friday, July 17, 2026 to be addressed at the hearing.

Questions about Maryland’s rate review process should be directed to Brad Boban, Chief Actuary at 410-468-2041, or by email.

Advertisement